The Trigger For The Next Great Depression

Aug 14, 2022 20:33:20 GMT -5

Post by J.J.Gibbs on Aug 14, 2022 20:33:20 GMT -5

The Trigger For The Next Great Depression

BY DOHMEN CAPITAL RESEARCH

SATURDAY, AUG 13, 2022 - 10:31

By Bert Dohmen, Founder

Dohmen Capital Research

During the bear markets of the past 30 years, inflation pressures were subdued, and therefore, the record money creation of the past 10 years apparently did not cause a visible problem. Inflation lags money creation.

However, inflation has now broken out to the upside and hit the highs established in 1980 to 1982. If the Fed now were to stimulate the markets with another round of excessive money printing, for the purpose of avoiding a recession till next year, inflation would go to the all-time record high of 1917, which is when the CPI soared over 19%.

From 2008 to 2018, the Fed increased its balance sheet (money printing) by five times (5x) Since that time it has doubled again through mid-2022 so now it is 10x the size of what it was in 2008. That is crazy and irresponsible, to say the least!

Monetary history of 2000 years shows that this dilution of the purchasing power of legal tender always ends in disaster.

This is the kind of thing that creates hyperinflation.

However, economists, top Federal Reserve officials, and politicians assure us that inflation is a temporary situation and will decline soon. They don’t say why or how. But they did pass a humongous $739 billion spending bill with big tax increases.

They celebrated on the floor of Congress when it passed, with backslapping and “high-fives.” It was even falsely labeled the “Inflation Reduction Act.” Little do they know that they passed an act that will be the trigger for the next “Great Depression” in the US.

This is so reminiscent of 1979, when inflation went to double-digits, but is now actually worse. In our Wellington Letter in 1979 we forecast the prime rate to go to 20%, but a top Wall Street economist called that “absurd.” The following year in 1980, the prime rate hit 20%.

Over the past 12 years the artificial money creation in major economies has soared to record historic highs. It is no longer just a US problem, it’s a global problem.

Money Supply M2, which we always followed closely, the past year hit a 40% rate. This has never been seen before. A rise of 8% used to be alarming. But now no analyst or economist bothers to mention the 40% growth rate. Is it that they don’t know, don’t think it is important, or are they trying not to scare investors?

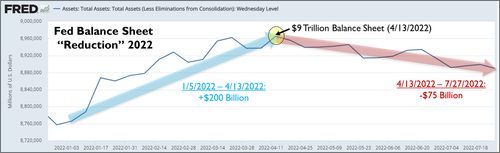

The Fed’s balance sheet reached an incredible, never thought possible, $9 trillion out of thin air earlier this year. That means that it has taken that much artificial money to keep the financial system glued together. That is exactly what is creating today’s big inflation. This is what Zimbabwe, Venezuela, and other hyperinflation countries have done.

Any educated person would say that the Fed has to stop what it is doing, lest prices go out of control. But the Fed chair has another concern: keeping his job and not being blamed for a big recession.

This year the Fed said it would tighten monetary policy to fight inflation. We have learned over the last 45 years to never trust what the Fed says. What they actually do is often the very opposite of what they say.

Remember that earlier this year, the Fed said it was going to “reduce its balance sheet.” That means it would reduce the record trillions of dollars of artificial money and credit creation of the past several years. The money creation has been the propellant of inflation, not Putin or greedy oil executives. But so far they have hardly reduce its balance sheet at all.

Inflation is manufactured at the Federal Reserve in Washington.

The effective remedy to fight inflation requires actions that will shrink credit and money supply. Both remedies will create a juicy recession and deep bear market in stocks, according to the “Dohmen Theory of Liquidity and Credit.”

Eventually, the Fed will have to make that difficult decision. Currently they seem to be “hoping” that inflation might decline through an act of nature. But wishful thinking doesn’t cure the inflation disease. And when the economic recession is finally recognized, the Fed may be urged to step on the accelerator again to prevent an overdue recession.

We often hear “hope” from Fed officials, economists and analysts. But that is a very ineffective tool. It is an act of desperation when you have painted yourself into a corner.

We consider inflation the most important economic factor. Again, the only way it can be fought is by contracting liquidity and reducing credit. But central banks hesitate to do it as it causes financial markets to plunge, and economies to go into deep recessions.

Therefore, central banks typically just hike interest rates, thinking that will reduce inflation as it may reduce borrowing. That is wrong if borrowing is still possible. Higher interest rates cause a rise in the cost of business, which is then passed on in the form of higher prices.

Tight (unavailable) money is the only way to get inflation down. But that is bitter medicine to cure the sins of the past.

Current inflation has wiped out any employment income gains. Yet people still pay taxes on the inflation-generated income. That’s why politicians like it: inflation is the silent tax. And if people can’t pay the higher tax, there will be an additional 87,000 enforcers soon enough at the IRS, waiting to pounce.

If the Congress were serious in helping Americans, they would cut taxes. For example, they would adjust capital gains tax on the sale of your home for inflation. A house bought 50 years ago, now sold at 10 times its original purchase price, has most of the gains because of inflation. It is not a profit!

Homeowners think they have done very well. But if they sell, they have to pay big taxes on the illusionary profit. From early 2009, the median priced home was $208,000. The next 11 years, to early 2020, it rose to $322,000.

That’s a gain of $114,000 in 11 years. Not bad.

But from early 2020 to early 2022, just two years later, that priced soared to $428,000, for a gain of $106,000 in just two years. Or a total gain of $220,000 in 14 years. However, that is not a profit because a new house would cost you that much…or more.

Here is the chart from the Fed showing how the median sales price for homes has skyrocketed since 2020:

Economic history shows that tax hikes produce recessions or depressions. President Harding got out of the post-WWI depression by ignoring the advice of his advisors, who urged more spending and higher taxes.

Instead, Harding cut government spending in half, cut taxes substantially, and reduced regulations. That created the prosperous period of the “Roaring Twenties.”

When the 1930’s recession started, Roosevelt did the opposite of Harding, cranking up the top tax rate over 90%. He created a 10-year depression out of what could have been a normal recession.

That lesson is now forgotten. However, if you want to survive the next 8 years, prepare now. The trigger for the next depression was pulled on Sunday, August 7, 2022.

link

BY DOHMEN CAPITAL RESEARCH

SATURDAY, AUG 13, 2022 - 10:31

By Bert Dohmen, Founder

Dohmen Capital Research

During the bear markets of the past 30 years, inflation pressures were subdued, and therefore, the record money creation of the past 10 years apparently did not cause a visible problem. Inflation lags money creation.

However, inflation has now broken out to the upside and hit the highs established in 1980 to 1982. If the Fed now were to stimulate the markets with another round of excessive money printing, for the purpose of avoiding a recession till next year, inflation would go to the all-time record high of 1917, which is when the CPI soared over 19%.

From 2008 to 2018, the Fed increased its balance sheet (money printing) by five times (5x) Since that time it has doubled again through mid-2022 so now it is 10x the size of what it was in 2008. That is crazy and irresponsible, to say the least!

Monetary history of 2000 years shows that this dilution of the purchasing power of legal tender always ends in disaster.

This is the kind of thing that creates hyperinflation.

However, economists, top Federal Reserve officials, and politicians assure us that inflation is a temporary situation and will decline soon. They don’t say why or how. But they did pass a humongous $739 billion spending bill with big tax increases.

They celebrated on the floor of Congress when it passed, with backslapping and “high-fives.” It was even falsely labeled the “Inflation Reduction Act.” Little do they know that they passed an act that will be the trigger for the next “Great Depression” in the US.

This is so reminiscent of 1979, when inflation went to double-digits, but is now actually worse. In our Wellington Letter in 1979 we forecast the prime rate to go to 20%, but a top Wall Street economist called that “absurd.” The following year in 1980, the prime rate hit 20%.

Over the past 12 years the artificial money creation in major economies has soared to record historic highs. It is no longer just a US problem, it’s a global problem.

Money Supply M2, which we always followed closely, the past year hit a 40% rate. This has never been seen before. A rise of 8% used to be alarming. But now no analyst or economist bothers to mention the 40% growth rate. Is it that they don’t know, don’t think it is important, or are they trying not to scare investors?

The Fed’s balance sheet reached an incredible, never thought possible, $9 trillion out of thin air earlier this year. That means that it has taken that much artificial money to keep the financial system glued together. That is exactly what is creating today’s big inflation. This is what Zimbabwe, Venezuela, and other hyperinflation countries have done.

Any educated person would say that the Fed has to stop what it is doing, lest prices go out of control. But the Fed chair has another concern: keeping his job and not being blamed for a big recession.

This year the Fed said it would tighten monetary policy to fight inflation. We have learned over the last 45 years to never trust what the Fed says. What they actually do is often the very opposite of what they say.

Remember that earlier this year, the Fed said it was going to “reduce its balance sheet.” That means it would reduce the record trillions of dollars of artificial money and credit creation of the past several years. The money creation has been the propellant of inflation, not Putin or greedy oil executives. But so far they have hardly reduce its balance sheet at all.

Inflation is manufactured at the Federal Reserve in Washington.

The effective remedy to fight inflation requires actions that will shrink credit and money supply. Both remedies will create a juicy recession and deep bear market in stocks, according to the “Dohmen Theory of Liquidity and Credit.”

Eventually, the Fed will have to make that difficult decision. Currently they seem to be “hoping” that inflation might decline through an act of nature. But wishful thinking doesn’t cure the inflation disease. And when the economic recession is finally recognized, the Fed may be urged to step on the accelerator again to prevent an overdue recession.

We often hear “hope” from Fed officials, economists and analysts. But that is a very ineffective tool. It is an act of desperation when you have painted yourself into a corner.

We consider inflation the most important economic factor. Again, the only way it can be fought is by contracting liquidity and reducing credit. But central banks hesitate to do it as it causes financial markets to plunge, and economies to go into deep recessions.

Therefore, central banks typically just hike interest rates, thinking that will reduce inflation as it may reduce borrowing. That is wrong if borrowing is still possible. Higher interest rates cause a rise in the cost of business, which is then passed on in the form of higher prices.

Tight (unavailable) money is the only way to get inflation down. But that is bitter medicine to cure the sins of the past.

Current inflation has wiped out any employment income gains. Yet people still pay taxes on the inflation-generated income. That’s why politicians like it: inflation is the silent tax. And if people can’t pay the higher tax, there will be an additional 87,000 enforcers soon enough at the IRS, waiting to pounce.

If the Congress were serious in helping Americans, they would cut taxes. For example, they would adjust capital gains tax on the sale of your home for inflation. A house bought 50 years ago, now sold at 10 times its original purchase price, has most of the gains because of inflation. It is not a profit!

Homeowners think they have done very well. But if they sell, they have to pay big taxes on the illusionary profit. From early 2009, the median priced home was $208,000. The next 11 years, to early 2020, it rose to $322,000.

That’s a gain of $114,000 in 11 years. Not bad.

But from early 2020 to early 2022, just two years later, that priced soared to $428,000, for a gain of $106,000 in just two years. Or a total gain of $220,000 in 14 years. However, that is not a profit because a new house would cost you that much…or more.

Here is the chart from the Fed showing how the median sales price for homes has skyrocketed since 2020:

Economic history shows that tax hikes produce recessions or depressions. President Harding got out of the post-WWI depression by ignoring the advice of his advisors, who urged more spending and higher taxes.

Instead, Harding cut government spending in half, cut taxes substantially, and reduced regulations. That created the prosperous period of the “Roaring Twenties.”

When the 1930’s recession started, Roosevelt did the opposite of Harding, cranking up the top tax rate over 90%. He created a 10-year depression out of what could have been a normal recession.

That lesson is now forgotten. However, if you want to survive the next 8 years, prepare now. The trigger for the next depression was pulled on Sunday, August 7, 2022.

link